Commercial debt collection is a common practice among companies these days.

Whether you’re a small business climbing up the ladder or have made it to the top and want to streamline things as much as possible, commercial debt collection should be your priority.

Yet, why is managing unpaid accounts so important for your business?

For starters, it can severely affect your cash flows, dictate your credit rating, and evaluate whether your business has operational stability or not.

Moreover, neglecting unpaid accounts can also lead to financial strain and legal complications.

But to make sure your business is on the right track, it’s equally important to be familiar with commercial debt collection terms and identify the exact things your business needs to cover all the gaps.

Starting With The Basics – Commercial Debt Collection Terms

Without getting into too much depth, we’ll first start with the most common and widely used commercial debt collection terms. These terminologies are based on the primary parties and the account involved:

Who Are Creditors and Debtors?

While the names might’ve given it away, it’s still best to get formally acquainted with these terms and to understand the debtor and creditor meanings.

- Debtor: A debtor is a person or an entity that owes money to a creditor ( A business that has taken out a loan)

- Creditor: A person or entity to whom money is owed (Example: A bank or vendor).

Moving past the debtor and creditor meaning, it’s also important to understand the dynamics of these together in commercial debt collection, their rights, responsibilities, and how to best navigate each role.

Roles:

- A Debtor is an entity or an individual who receives the requested funds, goods, or services from the creditor and thus owes compensation to the creditor. Due to this, they can have a significant impact on the creditor’s cash flow if the pending invoices are not cleared on time.

- A Creditor, on the other hand, provides funds, goods, or services requested by the debtor. They are responsible for keeping track of accounts and ensuring the payments are collected on time.

Rights:

- A Debtor can dispute claims made by the creditors under the assumption that the claims made on the debt are false or incorrect. They are also entitled to receive clear communication and notices before any efforts or legal action is taken by the creditors.

- A Creditor has the right to get paid on time, with any interest or fee included as per prior agreement. If the debtor fails to pay, the creditor can pursue legal action or collaborate with a collections agency as well. If the issue is not resolved, the case can even be reported to credit bureaus as well.

Responsibilities:

- A Debtor should pay their debts on time according to agreed terms. Moreover, they are responsible for proactively communicating any payment delays or issues. The debtors should also raise legitimate concerns or disputes promptly. Keep copies of invoices, contracts, and payments.

- A Creditor is responsible for providing clear credit terms, maintaining accurate records, and sending timely invoices and reminders. They must respond to debtor inquiries, enforce payment terms, and engage in fair collection practices. Additionally, creditors may offer payment solutions, report debts to credit bureaus, and comply with legal regulations. If necessary, they can pursue legal action for debt recovery.

If these terms are a bit too much for you and you’re looking to polish of some of your basics, then check out our blog Introduction to Commercial Debt Collection.

Tired of losing money in commercial debt collection?

How To Identify Delinquent Accounts In Business

Delinquent accounts in business refer to an account where the debtor has failed to make a payment by the due date. Delinquency, as part of commercial debt collection terms, can be categorized based on the length of time the payment is overdue:

- 30 days overdue: A gentle reminder may suffice.

- 60 days overdue: A more formal notice is recommended.

- 90+ days overdue: Consider escalating to a collection agency or legal action.

Regularly monitoring accounts receivable and promptly addressing overdue payments can help prevent accounts from becoming severely delinquent.

Recovering delinquent accounts can be a tedious task, especially when you have to navigate through the legalities and regulations involved in commercial debt collection. If you’re looking for a platform that can automate the whole process for you, then CollectCo is the perfect choice. Our automated recovery platform not only boosts your cashflow but also helps ensure you stay ahead of the curve without your accounts receivable aging up.

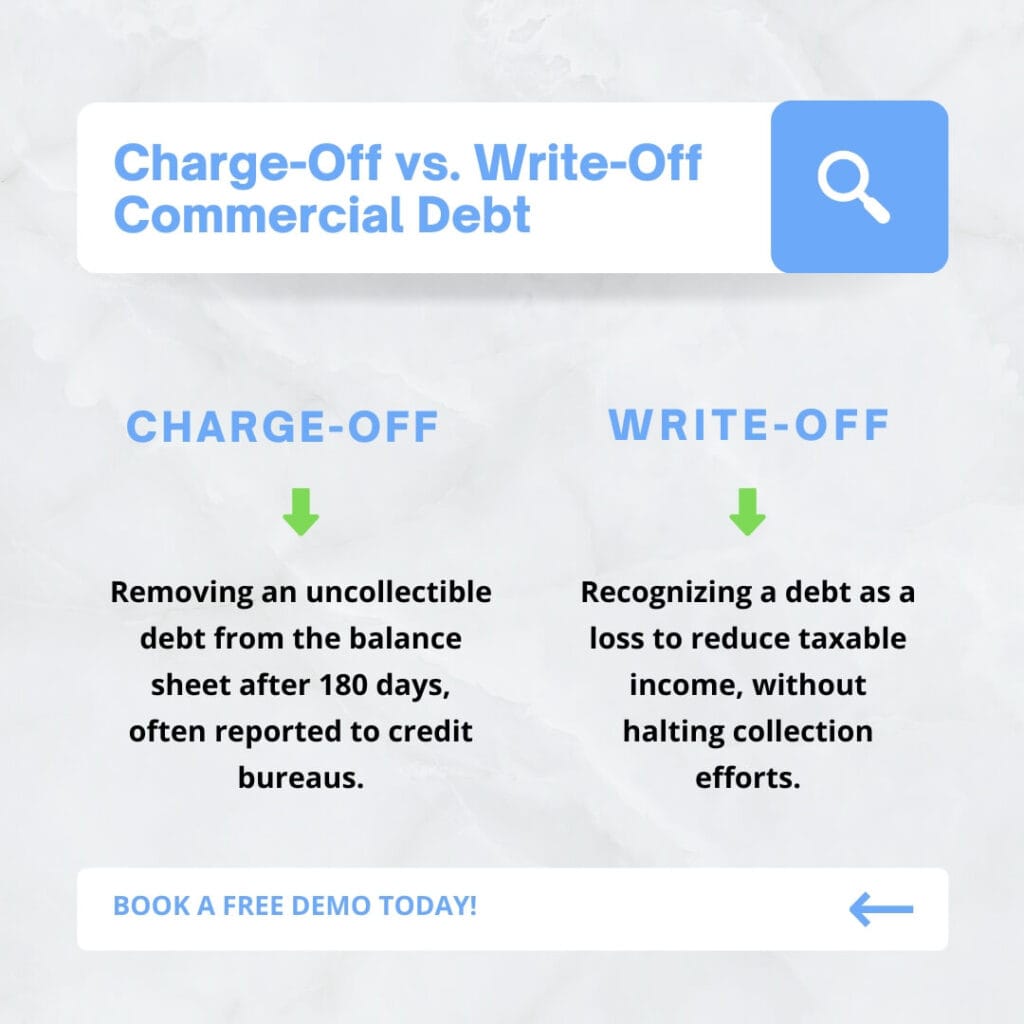

Charge-Off vs. Write-Off Commercial Debt

When debts become uncollectible, businesses must decide how to account for them:

Understanding the distinction between charge-offs and write-offs is crucial for accurate financial reporting and tax purposes as part of the key commercial debt collection terms.

Secured vs. Unsecured Debt Commercial Debt: The Role of Collateral

Debts can be classified based on whether they are backed by collateral:

- Secured Debt: This type of debt is backed by an asset (e.g., property or equipment). If the debtor defaults, the creditor has the right to seize the asset to recover the amount owed.

- Unsecured Debt: This debt isn’t backed by any collateral. If the debtor defaults, the creditor must pursue other means, such as legal action, to recover the debt.

Understanding the difference between secured and unsecured debt helps in assessing risk and determining appropriate collection strategies.

What Are UCC Filings For Debt Recovery?

To protect their interests, creditors may place legal claims on a debtor’s assets:

- Lien: A legal right or interest that a creditor has in the debtor’s property, lasting until the debt obligation is satisfied.

- UCC Filing: Under the Uniform Commercial Code, a creditor can file a UCC-1 Financing Statement(1) to establish a legal claim on specific assets, providing a public record of the creditor’s interest.

These tools can enhance a creditor’s ability to recover debts, especially in cases of default.

Default Notices In Commercial Debt

A default notice is a formal communication sent to a debtor indicating that they have failed to meet the terms of the debt agreement. It’s typically the first step and one of the more important commercial debt collection terms in the recovery process, and serves as a reminder of the outstanding obligation. Crafting a clear and professional default notice is essential for maintaining a positive business relationship while asserting your rights.

If your business is in need of crafting a clear and professional default notice is essential for maintaining a positive business relationship while asserting your rights, then CollectCo has got you covered. Our platform boasts 31+ years of experience in commercial debt collection that guarantees success without the risk of bad debt.

Understanding the Commercial Debt Statute of Limitations

The commercial debt statute of limitations refers to the legal time limit within which a creditor can initiate a lawsuit to collect a debt. This time frame varies by state, typically ranging from 3 to 6 years, but can be extended under certain conditions, such as written acknowledgments or partial payments.

Understanding your state’s statute of limitations is critical because once this period expires, the debtor may no longer be legally obligated to pay, even if the debt remains on record. Creditors should act promptly and document communication carefully to avoid losing legal leverage.

Tip: Always verify your jurisdiction’s commercial statute timelines before initiating collection proceedings.

Commercial Debt Restructuring – Negotiations 101

In some cases, rather than pursuing aggressive collection tactics, creditors may opt for debt restructuring. This involves renegotiating the terms of the debt agreement to make repayment more manageable for the debtor. Options may include extending the repayment period, reducing the interest rate, or offering a settlement amount. Debt restructuring can be a win-win solution, preserving the business relationship and increasing the likelihood of debt recovery.

What Is a Bad Debt Reserve and How Is It Calculated?

A bad debt reserve (or allowance for doubtful accounts) is a financial estimate used to account for receivables that are unlikely to be collected. Businesses calculate this reserve to reflect more accurate revenue and reduce financial risk.

Common methods to calculate a bad debt reserve include:

- Percentage of Sales Method(2): Based on historical default rates (e.g., 3% of credit sales).

- Aging of Accounts Receivable(3): Estimating uncollectible debts based on how long invoices have been outstanding.

This reserve is critical for financial reporting and helps businesses prepare for potential losses while staying compliant with accounting standards.

Commercial Debt Liens Explained

A lien is a powerful legal tool in commercial debt recovery. It grants a creditor the right to seize a debtor’s property if the debt remains unpaid. Here are the main types of liens in commercial debt:

- Judgment Lien: Placed after a creditor wins a lawsuit against the debtor.

- Statutory Lien: Arises by law, such as tax liens.

- Consensual Lien: Created by an agreement between the debtor and creditor (e.g., a mortgage).

Liens establish priority of repayment, meaning a creditor with a valid lien may have a legal claim over other unsecured creditors when assets are liquidated.

Acceleration Clauses: Enforcing Immediate Repayment

An acceleration clause is a provision in a debt agreement that allows the creditor to demand the full repayment of the outstanding balance if certain conditions are met, such as missed payments or breach of contract. This clause provides creditors with a mechanism to expedite debt recovery and protect their financial interests.

Guarantor Liability: Holding Third Parties Accountable

In some debt agreements, a third party, known as a guarantor, agrees to be responsible for the debt if the primary debtor defaults. Understanding the rights and obligations of a guarantor is crucial, as they can be held liable for the debt, potentially leading to legal action if the primary debtor fails to pay.

Debt Settlement vs. Bankruptcy: Exploring Options

When faced with uncollectible debts, creditors may consider:

- Debt Settlement: Negotiating with the debtor to accept a reduced amount as full payment. This can be a quicker and less costly alternative to legal action.

- Bankruptcy: A legal process where a debtor declares their inability to repay debts. Bankruptcy can result in the discharge of certain debts but may also involve asset liquidation.

Each option has its pros and cons, and the best choice depends on the specific circumstances of the debt and the debtor’s financial situation.

Is your business struggling with unpaid debts?

Commercial Debt Collection Glossary

To help you navigate the terms discussed in this guide, we’ve compiled a quick glossary of essential commercial debt collection terms.

- Debtor: A person or business that owes money to another party (the creditor).

- Creditor: A person or business to whom money is owed by the debtor.

- Delinquent Account: An account that has not been paid by its due date and is considered overdue. Delinquent accounts are typically categorized into 30, 60, or 90+ days overdue.

- Charge-Off: The act of removing an uncollectible debt from a company’s balance sheet after a specified period of nonpayment, usually 180 days.

- Write-Off: A process of recognizing an uncollectible debt in the company’s financial records as a loss but not necessarily ceasing collection efforts.

- Secured Debt: Debt backed by collateral. If the debtor defaults, the creditor can seize the collateral to recover the owed amount.

- Unsecured Debt: Debt that is not backed by collateral, making it riskier for creditors and more challenging to recover.

- Lien: A legal claim or right on a debtor’s property held by a creditor, which remains in effect until the debt is paid.

- UCC Filing: A filing made under the Uniform Commercial Code (UCC) to establish a legal claim on assets used as collateral in a commercial debt agreement.

- Default Notice: A formal notice sent to a debtor indicating that they have failed to meet the terms of their debt agreement.

- Debt Restructuring: Renegotiating the terms of a debt agreement to make it more manageable for the debtor, often involving extended repayment periods or reduced interest rates.

- Acceleration Clause: A provision in a debt contract that allows a creditor to demand immediate full repayment if certain conditions are met, such as missed payments.

- Guarantor: A third party who agrees to pay a debt if the primary debtor defaults.

- Debt Settlement: A process in which a debtor negotiates to pay a reduced amount of the total debt to settle the obligation.

- Bankruptcy: A legal process in which a debtor declares the inability to repay debts and seeks legal protection. It can involve the liquidation of assets or the restructuring of debts.

Conclusion

Understanding the key terms in commercial debt collection is essential for effectively managing overdue accounts and protecting your business’s financial health. By familiarizing yourself with concepts like debtor and creditor roles, delinquent accounts, charge-offs, secured and unsecured debts, and legal tools such as liens and UCC filings, you can navigate the complexities of debt recovery with confidence.

Remember, proactive management and clear communication are vital in preventing and addressing overdue payments. By implementing sound credit policies, monitoring accounts receivable regularly, and understanding your rights and options, you can enhance your business’s cash flow and reduce the risk of bad debts.

If you found this guide helpful and would like to delve deeper into specific aspects of commercial debt collection, feel free to explore our other resources or contact us for personalized advice and assistance.

FAQs

What is commercial debt collection, and why is it important?

- Commercial debt collection is the process of recovering outstanding debts owed by businesses. It is essential for maintaining healthy cash flow, preserving business relationships, and ensuring financial stability.

What are the rights of a debtor in commercial debt collection?

- Debtors have the right to dispute claims, receive clear communication, and be informed of any legal actions before proceeding. Understanding debtor rights helps prevent unfair collection practices.

How can delinquent accounts be identified in commercial debt collection?

- Delinquent accounts are typically identified when payments are overdue beyond the agreed terms, often categorized as 30, 60, or 90+ days overdue. Managing delinquent accounts promptly helps prevent further financial strain.

What are the differences between charge-offs and write-offs in commercial debt?

- A charge-off is when a creditor deems the debt uncollectible but may continue efforts to recover it, while a write-off completely removes the debt from the financial records. Both affect the business’s financial statements.

How does a UCC-1 filing help in commercial debt recovery?

- A UCC-1 filing secures a creditor’s interest in a debtor's assets, ensuring priority over other creditors if the debtor defaults. This legal tool is crucial for protecting creditor rights during debt recovery.